10 advantages of term life insurance & when should you buy it

10 advantages of term life insurance & when should you buy it

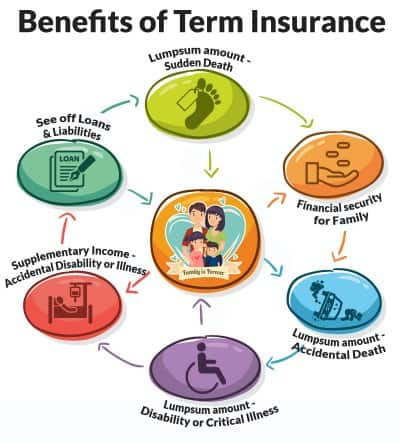

Advantages of term life insurance:

• SimplicityTerm insurance plans are much easier to understand than insurance plans such as endowment policies which combine risk cover with savings. Plans which comprise risk cover plus a savings component are also known as cash value plans. It is not always easy for a layperson to divide the premium he pays into risk cover cost and the amount actually being invested on his behalf as savings. Planning financial goals around a cash value insurance plan can get really complicated. There are rules governing things like the size of your cash value savings versus the policy death benefit and the repayment of policy loans etc. Term life, on the other hand, is the essence of simplicity - pay the premium and get covered for the term chosen.

• Competitive pricing

Term life policies can be easily compared with each other on the basis of price as they are structurally similar and also simple to understand. This has led to a very competitive market in which term life policies are rapidly becoming a "commodity". Buyers suffer fewer information problems with term insurance, thus rendering the term market more price-competitive than for cash value policies.

• FlexibilityOpting out of a term life policy is much easier than getting out of cash value policies. In term policies if you stop paying the premium the risk cover ceases and the policy ends. Nothing is payable to you as there is no savings element in the policy. However, cash value policies only give the full promised survival benefit if they are held for the full tenure of the policy. If you stop paying premiums mid-term there is financial loss as you cannot recoup your savings portion of the policy without certain deductions.

Further, many term life policies are "renewable" and "convertible." The former ensures that you can go in for another term policy without a medical exam at the end of the first term policy. The latter allows you to convert your term life policy into an endowment policy for the same sum assured with associated increase in premium, should this make sense during the term of the policy.

• Tax benefitIt is often argued that if you buy endowment type of insurance, as the premium is more you get more benefit u/s 80C of the Income Tax Act while investing. Additionally, it also yields tax-free income when the maturity claim is paid. However, it needs to be pointed out that while premium paid for term insurance is much less it is also eligible for tax benefit u/s 80C. Further, the difference in premium between term and endowment insurance can also be invested in some other tax efficient schemes like PPF, ELSS which also offer front and rear end tax breaks similar to those offered by an endowment plan.

• Lowest premiumsThe premium for term insurance is much lower than that for comparative cash value policies. For example, currently it is possible for a 30-year old person to buy a level term insurance policy of 20 years for Rs 10 lakh sum assured for about Rs 3000 annual premium. For an endowment policy without profits, with exactly the same death benefit, the premium will be a little above Rs 30,000 annually. For an endowment policy with profits, the yearly premium will be about Rs 50,000.

Limitations of term insurance

Uses of Term Insurance

Uses of Term Insurance

Term Insurance policies will be most appropriate for the following life situations and needs:

• If your budget is tight then term insurance is a better option as cash value insurance costs much more.

• Tax benefitIt is often argued that if you buy endowment type of insurance, as the premium is more you get more benefit u/s 80C of the Income Tax Act while investing. Additionally, it also yields tax-free income when the maturity claim is paid. However, it needs to be pointed out that while premium paid for term insurance is much less it is also eligible for tax benefit u/s 80C. Further, the difference in premium between term and endowment insurance can also be invested in some other tax efficient schemes like PPF, ELSS which also offer front and rear end tax breaks similar to those offered by an endowment plan.

• Lowest premiumsThe premium for term insurance is much lower than that for comparative cash value policies. For example, currently it is possible for a 30-year old person to buy a level term insurance policy of 20 years for Rs 10 lakh sum assured for about Rs 3000 annual premium. For an endowment policy without profits, with exactly the same death benefit, the premium will be a little above Rs 30,000 annually. For an endowment policy with profits, the yearly premium will be about Rs 50,000.

Limitations of term insurance

- The premium for term insurance steeply increases with advancing age and hence insurance needs at higher ages cannot be economically met with term insurance.

- At older ages, say beyond 65 or 70 it becomes difficult to buy term insurance as most companies do not offer it beyond these ages. Even in cases where term insurance is offered at ages beyond this, several conditions, disadvantageous to the insured, are attached.

- Term insurance will not serve the purpose if you wish to save money for a specific need such as education of child, marriage, old age provision like retirement needs etc.

- It will also not help you provide for income or capital needs of your family while you are living.

- No surrender values or loans are available under term policies.

- Term insurance cannot provide a hedge against inflation as they are without profit plans.

- In case you become uninsurable at any point of time due to health or other reasons then new term insurance or renewal of an existing term policy will not be available.

- Wealth creation is not possible through term insurance.

Term Insurance policies will be most appropriate for the following life situations and needs:

• If your budget is tight then term insurance is a better option as cash value insurance costs much more.

Term insurance would also be suitable for a person with low income but requiring a large cover to protect his family's financial future in case of his demise. For similar reasons, this type of insurance would also suit a person who is the sole breadwinner in the family and has moderate income.

• Persons on the threshold of new careers or business ventures can save on costs by buying term insurance instead of a cash value policy so that they can utilize their balance income or capital to develop their career or business.

• Term insurance is also suitable if you have taken a large loan such as housing loan, car loan etc. Further, it is relevant persons who have invested substantially in new ventures by borrowing at high interest rates or by mortgaging their property. Such persons can cover the risk of their dying before repaying all loans by taking term insurance which is cheaper than the other types of insurance.

• Term insurance can also be used by employers to provide life cover to their employees - particularly the labour class - as a welfare measure at low cost. What is more, companies can claim the premium paid on such policies as a business expense.

• Term insurance can be used to ensure future insurability. A person who desires large amount of cash value insurance may be financially unable to pay for it immediately. Inexpensive term insurance can be conveniently converted to cash value insurance later on, when the capacity to pay improves. Generally, when a term plan is converted into an endowment plan,

• Term insurance can be a supplement to endowment and whole life policies in a well rounded financial plan designed taking into account the capital and income needs of an individual. For example, term insurance can be used as a rider to a cash value insurance policy in order to increase death cover for a specific time period e.g. when a loan has been taken and has to be repaid.

• Persons on the threshold of new careers or business ventures can save on costs by buying term insurance instead of a cash value policy so that they can utilize their balance income or capital to develop their career or business.

• Term insurance is also suitable if you have taken a large loan such as housing loan, car loan etc. Further, it is relevant persons who have invested substantially in new ventures by borrowing at high interest rates or by mortgaging their property. Such persons can cover the risk of their dying before repaying all loans by taking term insurance which is cheaper than the other types of insurance.

• Term insurance can also be used by employers to provide life cover to their employees - particularly the labour class - as a welfare measure at low cost. What is more, companies can claim the premium paid on such policies as a business expense.

• Term insurance can be used to ensure future insurability. A person who desires large amount of cash value insurance may be financially unable to pay for it immediately. Inexpensive term insurance can be conveniently converted to cash value insurance later on, when the capacity to pay improves. Generally, when a term plan is converted into an endowment plan,

• Term insurance can be a supplement to endowment and whole life policies in a well rounded financial plan designed taking into account the capital and income needs of an individual. For example, term insurance can be used as a rider to a cash value insurance policy in order to increase death cover for a specific time period e.g. when a loan has been taken and has to be repaid.

Term Life Insurance Advantage No. 1Term insurance allows a person to acquire the greatest death benefit for the lowest premium outlay when the policy is first issued. However, this does not mean that term insurance is necessarily the least expensive form of insurance over the full duration of needed coverage. Because term premiums increase at each renewal, at the later ages the premium cost will far exceed the level premium that would have been charged for an ordinary whole life policy issued at the same age as the original term policy.

Term Life Insurance Advantage No. 2Term insurance is the best alternative for temporary life insurance needs. Usually term insurance is the best alternative if protection is needed for less than ten years. Conversely, some form of cash value life insurance will generally be the best alternative if protection must continue for fifteen or more years. If the duration of the needed protection is between ten and fifteen years, the best alternative depends upon the facts and circumstances of the case. As a general rule of thumb, term insurance will tend to be better than cash value insurance at issue ages below age forty-five, and worse at older issue ages if the length of the need for protection is between ten and fifteen years.

Term Life Insurance Advantage No. 3Younger persons may acquire substantial face amounts of coverage at relatively low immediate cost, perhaps more than their immediate needs, and thereby guarantee that they will have the necessary level of coverage when their needs and family obligations later increase, even if they are then uninsurable.

Term Life Insurance Advantage No. 2Term insurance is the best alternative for temporary life insurance needs. Usually term insurance is the best alternative if protection is needed for less than ten years. Conversely, some form of cash value life insurance will generally be the best alternative if protection must continue for fifteen or more years. If the duration of the needed protection is between ten and fifteen years, the best alternative depends upon the facts and circumstances of the case. As a general rule of thumb, term insurance will tend to be better than cash value insurance at issue ages below age forty-five, and worse at older issue ages if the length of the need for protection is between ten and fifteen years.

Term Life Insurance Advantage No. 3Younger persons may acquire substantial face amounts of coverage at relatively low immediate cost, perhaps more than their immediate needs, and thereby guarantee that they will have the necessary level of coverage when their needs and family obligations later increase, even if they are then uninsurable.

Term Life Insurance Advantage No. 4The conversion feature of renewable and convertible term allows policyholders to enjoy higher death protection than they could otherwise afford and later allows them to lock-in their premiums and build cash values when their ability to pay premiums increases.

Term Life Insurance Advantage No. 5Various types of term insurance — level, decreasing, and increasing — can be combined as riders with other types of permanent insurance to create a package that meets a person’s special death protection, savings, and affordability needs.

Term Life Insurance Advantage No. 6Life insurance proceeds are not part of the probate estate, unless the estate is named as the beneficiary of the policy. Therefore, the proceeds can be paid to the beneficiary without any delay caused by administration of the estate.

Term Life Insurance Advantage No. 7There is no public record of the death benefit amount or to whom the death benefit is payable (if paid to someone other than the deceased’s estate).

Term Life Insurance Advantage No. 8The death benefit proceeds are generally not subject to federal income taxes.

Term Life Insurance Advantage No. 9The death benefit proceeds are often exempt from state inheritance taxes.

Term Life Insurance Advantage No. 10Life insurance policies can be used as collateral or security for personal loans. Although lenders generally prefer permanent types of policies because of the cash values, a term policy is often sufficient if the borrower is a good credit risk and the loan is very likely to be repaid unless he or she dies.

Term Insurance Plans offered by Insurance Companies All You Should Know

- Edelweiss Tokio Term Insurance Co. Ltd.

- Future Generali India Term Insurance

- HDFC Standard Term Insurance

- Max Life Term Insurance

- LIC Term Insurance

- SBI Term Insurance

- Tata AIA Term Insurance

- Aviva Term Insurance

- Bajaj Allianz Term insurance

- Aegon Life Term Insurance

- Reliance Nippon Term Insurance

- Sahara Term Insurance

- Bharti Axa Term Insurance

- Birla Sun Life Term Insurance

- Canara Hsbc Term Insurance

- Dhfl Pramerica Term Insurance

- Exide Life Term Insurance

- IDBI Federal Term Insurance

- Indiafirst Term Insurance Kotak Term Insurance

- Star Union Dai Ichi Term Insurance

- PNB Metlife Term Insurance

Visit For Comparing termplan

POPULAR TAGS SIP,ELSS,Mutual Funds,Retirement,Term Insurance,Motor Insurance,Health Insurance,Insurance,Save Tax,Tax Slabs,Income Tax

Post a Comment